Liquid hydrogen with new pumps reduces station boil-off by 50% – and LH2 is still not the solution

Bosch recently developed a Liquid Hydrogen (LH2) fueling pump that reduces hydrogen refueling station losses from boil-off by 50%. While this is a great step forward, unless liquefaction is made much less expensive and more efficient, this pump’s usefulness is questionable. The important take-away from this article is that liquid hydrogen station operators are finally owning up to the fact that LH2 has large leak issues that aren’t present with Gaseous Hydrogen (GH2).

The only true proponents of LH2 are vehicle manufacturing companies that want cryogenic LH2 on the vehicle– because it takes all the complexity away from them and shoves that complexity onto the balance sheets of energy infrastructure. For an existing vehicle company, Frankensteining in GH2 equipment into an existing vehicle avoids the clean-sheet development step, saving literally billions of dollars in one-off levels of development, testing, and regulation design. LH2 is much easier to Frankenstein into an existing frame design, making it much less expensive. LH2 prevents the vehicle company from building a one-off team to do a clean-sheet design on a new vehicle frame – which includes designing an entire factory and process to build the vehicle – but puts all the complexity and cost onto the infrastructure side. But LH2 is and likely always will be more expensive than GH2 in most cases. Shown here is recent analysis from an earlier post:

New gaseous H2 conditioning, distribution, and fueling systems are far more cost effective than liquid systems.

Ultimately, the current high cost and failure of delivery of H2 in California fueling is heavily owed to liquid hydrogen value chains. Developing robust and flexible gaseous hydrogen value chains have already fixed these issues in the EU. In the rest of this post, I explain some of the technical and techno-economic background of why liquid hydrogen is so expensive– the few locations and use cases where that expense is justified. But first, I discuss some of the history, and why incumbents and some newcomers are stuck on the moribund idea of LH2 fueling.

LH2 is less than 1% of current H2 markets - yet even Shell and others (erroneously) considered its potential for fueling

The entire world has a liquid hydrogen capacity of less than 1000 tons per day compared to the more than 300,000 tons per day that are moved through pipes for conventional hydrogen uses. Liquid hydrogen is a rounding error for a reason – it’s too expensive outside of edge cases. It’s not because liquefaction of hydrogen is new – hydrogen was first liquefied in 1898, only 12 years after natural gas was first liquefied. The liquefaction process has been CapEx and OpEx intensive for over half a century and hasn’t changed.

When I joined Shell Hydrogen, my first mandate was to create a commercial roadmap for Shell to determine whether they should get into liquid hydrogen for vehicle fueling or whether they should wait out the transition to commercial H2 pipelines existing. Shell was confident that if they wanted to scale liquid hydrogen and reduce cost, they could. After all, they were one of the largest successes of the LNG industry. Only one question remained: would the liquid hydrogen advantage be overcome rapidly by the development of pipelines, or would it be a waste of development dollars?

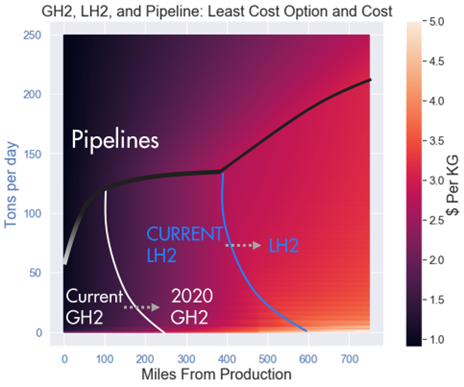

I built a techno-economic simulation in Python that would run thousands of times to compare moving hydrogen via gaseous trucks, with pipelines, as LH2, and with pipelines plus gaseous trucks for the last 50 miles. The results shown above are clear: with the new generation of compressors and carbon fiber trailers, not only was the timeline for liquid hydrogen being more cost-effective too limited for Shell, that timeline no longer existed. There is no world in which LH2 is more cost-effective than locally made GH2 unless that use case is a rocket. Hydrogen would need to be trucked over 250 miles one-way to be more cost effective as a liquid than a gas. The advent of autonomous trucking will make this distance effectively well over 1000 miles – since most of the cost is actually the truck driver. See rough costs here:

2020 analysis of the conditioning distribution break-even points between liquid, gasesous, and pipeline+gaseous truck deilvery of H2

Note that while the 50 year old LH2 supply chain became 2x the cost since 2020, gaseous equipment has gone down in price. This chart above needs to be updated, but the 2022 DOE Commercial Hydrogen Liftoff Report found concurring costs.

Not only did one of the most technically competent gas companies in the world miss this – so did the top research institutes in the US.

When I joined the US Department of Energy, both the DOE and the associated National Labssaw no path for gaseous hydrogen. Within a month, both were much more receptive to the change than industry at large. By the end of my first quarter, DOE consensus was that gaseous hydrogen was almost always the lowest cost way to move hydrogen, provided the proper equipment was used. This is why the DOE H2 commercial liftoff report, which was vetted by the entire DOE, indicated that gaseous systems were the lowest cost. There remained disagreement – but the disagreement wasn’t credible enough to strike the lower gaseous costs from the report.

Why did we get it wrong for 20 years?

The short answer is that Americans got it wrong and the EU has always done right. In the EU, functionally all hydrogen is moved in pipes or on GH2 trailers, even small-scale uses. In the US, however, more of the hydrogen for small use cases like vehicles is moved as liquid. This is in part because the Department of Transportation in the US requires steel tube trailers that are far more robust than in the EU – making it so that only 200kg can be moved on a steel trailer in the US vs 1,000kg in the EU. As a result, talk of liquid hydrogen fueling in the EU is non-existent on the credible H2 infrastructure side. Large LH2 projects languish in Memorandum of Understanding territory and don’t hit Final Investment Decision. Or they run themselves to near bankruptcy like Plug.

In both the US and EU, however, GH2 hydrogen compressors and pre-cooling were notoriously unreliable for two decades – often having up to 30% downtime even with 2x redundant compressors. Pre-cooling systems specifically were terrible, using 10kwh/kg because they kept a liquid cold and the energy leaked to the environment. Liquid hydrogen has to be warmed up to fuel, so pre-cooling isn’t an issue. New gaseous pre-coolers use much more efficient expansion cycles which use 5% of the power of the old ones, however.

I was the first one to model the new tube trailers and more reliable gaseous piston compressors, and the first to model offtake from an H2 pipeline to a compressor station for H2 trucks. These details made it clear that there really is no cost-effective large-scale use case for liquid hydrogen.

What makes liquid hydrogen so expensive?

It’s the liquefaction.

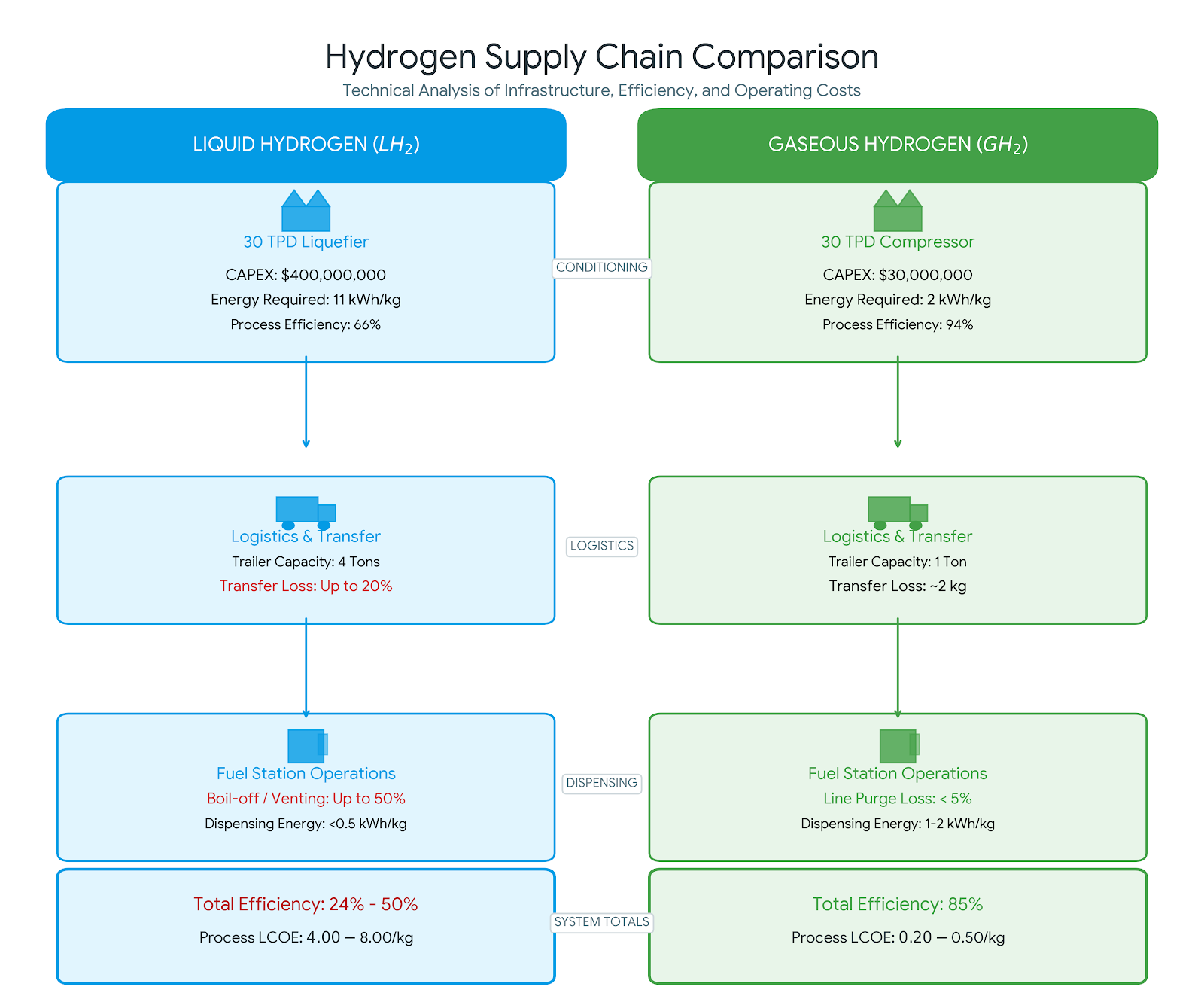

Diagram of major LH2 and GH2 CapEx and OpEx requirements

A liquefier is over 10x the cost of a compressor and requires 5x the energy – generating 6x the efficiency loss of simply compressing. The levelized cost and other figures above are from techno-economic analyses and went through a robust consensus process at the US Department of Energy for DOE’s commercial hydrogen liftoff report. Take other sources with a grain of salt.

Why do Shell and others still consider liquid hydrogen?

The major goal of large companies with LH2 is to cut out all other parties that would be required to make pipelines and thus GH2 to work. This allows moving energy between continents without dealing with any other entities except the buyer. This is easier to do over the ocean, where LH2 makes more sense than a pipeline. Compared to a ship on the ocean, building infrastructure over land is difficult and prone to failure and cancellations. Gaseous hydrogen pipelines would require the cooperation between many companies as well as governments at the city, state, and national levels. In comparison, LH2 can be loaded onto a ship in one country and delivered to a port in another by a single company. A large company like Shell could handle every aspect of the liquid hydrogen supply chain from production through transport and delivery.

In short – without the ability to build pipelines, and without the ability to locally produce cost-effective hydrogen – then liquid becomes the only option to move pure H2 between continents. Many large companies are banking on H2 backbone pipelines never coming to fruition.

Vehicle manufacturers will often push LH2 because it drastically reduces their cost and complexity - GH2 tanks don’t fit into current car designs and they don’t want to go through the massive expense of clean-sheet designs for a market that barely exists.

In which use cases does LH2 make sense?

The largest viable use of LH2 is delivering low-carbon energy from renewable-rich or CO2-storage rich countries to those with less or none of these resources. Making cost-effective hydrogen locally requires either low-cost power or low cost natural gas. If gas is expensive, however, like in the EU, it may be more cost effective to make the hydrogen where it is low cost and move it to the destination. Think of it this way: if Oman has $3/mmbtu gas and burns 33% of it to run a liquefier, the cost-efficiency hit is 33% of $3, or $1 extra. Liquefying in the EU with $20/mmbtu gas would be 33% increase on $20, or nearly $7. The same can be said for electricity – Morocco has far better solar costs than any part if Germany, so shipping may make more sense if no pipelines ever arise[1].

Another area that LH2 makes sense is urban fueling station forecourts. GH2 requires thick-walled tanks that take up as much as 3x the space of liquid hydrogen. Moreover, gaseous hydrogen trailers have to be swapped to be cost effective. In urban environments, delivering gaseous hydrogen via trailer swap and storing gaseous hydrogen has already proven challenging. Most fueling in the US, however, happens in suburban and highway environments where GH2 is perfectly suited.

Other use cases will be niche. In the EU, most LH2 is used in processes that require ultra purity, like semiconductors. Rockets use liquid hydrogen because the thrust per unit weight is great – but SpaceX switched to kerosene because LH2 is fickle and expensive. It turns out that SpaceX brought the cost to boost a ton of mass to space so much that the added mass of using kerosene is better than break-even.

Finally, vehicle racing applications may benefit from LH2 owing to the incredible power-to-weight ratio.

The high cost of LH2 will make it a niche use case in most end uses.

What if liquefiers became more cost effective? It won’t matter – the scale required to hit competitive prices with a pipeline are intercontinental – not continental

Plug already tried reducing liquefier costs and failed. It will take a super-major oil company to design at the scale required to make LH2 cost-effective. It is possible, but like natural gas, it will only be used to move energy between continents and any country that can produce its own H2 will move it in pipelines and trucks.

One final point to close – for GH2 fueling 350 bar or 500 bar make a lot more sense

I have bashed LH2 fueling quite a bit here, but current fueling paradigms for gaseous are also driven by the vehicle manufacturer’s laziness and not true physical constraints on the vehicle. While moving the GH2 is more cost-effective than LH2, 700 bar fueling requires industrial equipment. 350 bar fueling eliminates pre-cooling and most or even all compression at the gas station, and 500 bar fueling can eliminate most pre-cooling and drastically reduce compression required. Reducing or eliminating equipment at the fueling forecourt should be the primary goal of the industry – especially when the more complex processes can be put upstream at a fenced industrial site.

700 bar fueling has the same provenance as LH2 onboard a truck- vehicle companies saving money by pushing cost and complexity onto infrastructure. Lower fueling pressure makes much more sense across the board.

[1] We’re ignoring the “ammonia vs liquid hydrogen” debate here because large scale processes here to make H2 at the end use site are still low TRL.