Natural Gas Distribution Will Constrain Data Center Growth

In every power and energy industry I’ve worked with, nearly everyone forgets that electrons and molecules need to be moved around – and that maintaining excess capacity to move them around is very expensive. As a result, we only have vastly excessive distribution capacity if it is associated with abundant overbuilding that has left pile of bankrupt companies in the wake. Data center gas demand is the exact type of new energy demand that requires vast amounts of excess capacity that simply don’t exist and aren’t easy to build.

Natural gas distribution is going to become a bottleneck for data centers soon. Many new data center permits are operating under a “bring your own power” plan whereby they produce power on-site and largely bypass a grid connection. Most want natural gas. This nat-gas focus has already doubled the cost of natural gas turbines and increased the wait time on turbines to up to seven years.

While the US has extra production capacity for natural gas, buildings new distribution capacity in the form of pipelines will be difficult – or impossible.

Unrelieved constraints already exist in the US

In January 2026, New England burned 1.6 million barrels of oil for power generation over the course of nine days. This rate of ~200,000 barrels per day for a population of ~15M compares to the 220,000 barrels per day for the entire country of Saudi Arabia with 38M people. This means that the Northeast per-capita burned 200% of the oil for electricity that Saudi Arabia did, making it by some metrics the most oil-intensive power sector in the world for a week. Keep in mind that Saudi Arabia produces prodigious amounts of low-cost oil, and New England is not a known oil producing region, so this is staggering.

Once or twice per year the natural gas distribution capacity in New England is tapped out. The entirety of natural gas available is used for heating, largely in homes, and power plants still need fuel to provide electricity for those with electric heat just to keep people alive.

Enter the “dual fuel power plant” that can switch seamlessly from natural gas to heavy oil or diesel. During cold snaps, natural gas diverted to heating homes is unavailable for power plants, and the power plants switch to oil to provide power for the home heat that keeps electric heat users alive.

A rising solution in the Northeast is the purchase of Liquid Natural Gas (LNG) by ships, bypassing the pipelines to augment the natural gas supply in the region. LNG competes on a global market and can push above $20-30/mmbtu compared to pipeline natural gas prices that are closer to $3-$5/mmbtu during normal course of events (spot prices for pipeline gas spike far above this during cold snaps).

Natural gas storage isn’t a viable solution, and cost isn’t the issue for expanding pipeline capacity

The largest storage of natural gas in the US is the pipeline network. By packing pipelines with higher pressure, pipeline owners can store natural gas for later use. When the pipelines are drained and distribution is constrained, this storage is already depleted. Other types of storage – like geologic storage – are region-constrained with very few places in the US able to store gas.

LNG on a ship becomes the only way to “store” gas for major events. The all-in cost for an LNG terminal is on the order of $1B (for floating LNG) or $2B (for a land terminal). $2B could pay for 400 miles of a pipeline large enough to power an entire medium sized country or 1000 miles of a pipeline large enough to supply enough gas for all of New England. The reason we don’t build more pipelines is political – and can’t be circumvented.

This means higher costs for retail customers – IE families

Constrained supply increases the spot price of gas from a pipeline or from other sources. When the spot price of gas rises during emergencies, the gas and electricity prices rise as well. Utilities pass much of these prices on to the consumer – meaning higher gas and electricity bills.

We will see more local and regional natural gas constraints as data centers build out

The expansion of data centers heralds the expansion of natural gas use. In Northern Virginia, the densest area in the country for data centers, total increase in power demand for data is around 6GW active or under construction. This is enough power 4.5 million homes. This has led to a 93% increase in power costs in the Washington, DC area from 2020 to 2025. This is before any gas distribution constraints have arose in the area – and is also part of why new data centers are often expected to “bring your own power.” As data centers bring their own power production, they will vacuum up spare natural gas distribution capacity – raising prices further. This will make many areas more hostile to the construction of data centers.

Data center growth will be limited by this distribution bottleneck

Data centers need power and most regional grids have gotten wise to the fact that their power prices will increase dramatically, like in Washington DC area, if data centers don’t provide their own power. The only reliable fuel source currently is natural gas – new-build coal isn’t going to happen. Data center builders are looking for whatever natural gas power plants they can – going so far as to buy untested hardware from startups that have never delivered at scale. They are desperate to get power from gas as soon as possible – and many areas are already short on gas several times per year. As a result, data centers will have to focus growth in areas where there is natural gas production or the ability to build new pipelines.

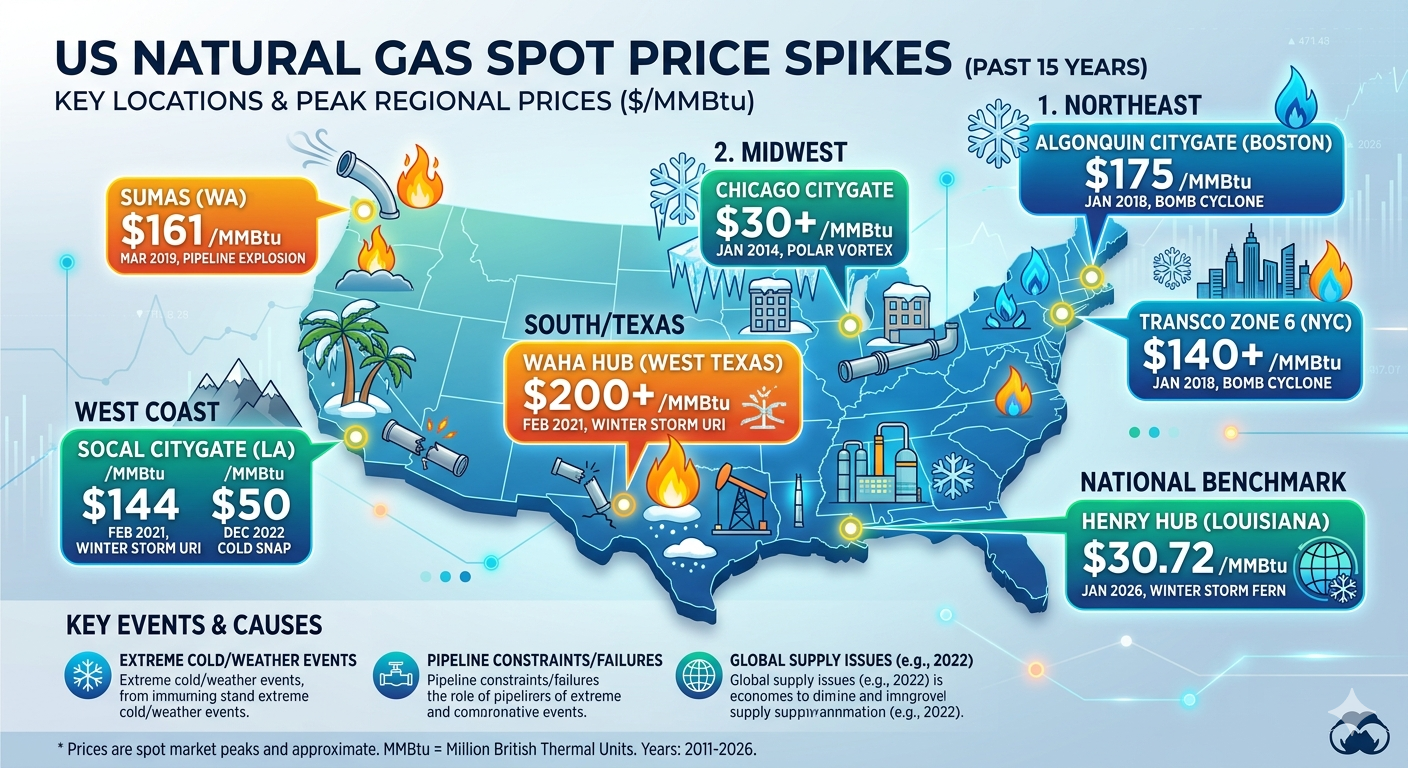

Where are regions that already have distribution restrictions?

This is solved by a quick search on locations where gas spot prices have spiked. During the last winter storm, the Northeast saw a 35% spike in natural gas demand and the power plants flipped to oil in response. We’ve seen several similar events over the course of the past decade:

Source: EIA data and graphic created with Google Gemini

It is pretty much inevitable that we will see gas prices rise across the US if data center demand hits targets

During the January 2026 winter storm, US gas demand rose 20% from the prior week. The Henry Hub prices spiked from an average of $7.75/mmbto to $30/mmbtu.

150GW of data center plans have been filed nationally. Current national natural gas demand for power is about 130-230GW, and this represents about half of total demand. If data center build out continues at pace, it will represent a 50% increase in demand for gas during good weather and a demand increase of over 25% during the worst weather that we’ve seen. A lower 20% spike in national demand increased Henry Hub prices by 400% in January 2026. While this January 2026 spike partially represents an inability to ramp production at that time, it moreso represents a lack of pipeline capacity. Remember – pipelines store gas by packing the pipelines with higher pressure. Supply constraints that push Henry Hub to $30/mmbtu are indicative of the fact that we drained much of the US natural gas pipeline network in the constrained areas. Production and storage is integrated over time, and we blew through the capacity we had in the east coast of the US with just a 20% demand increase in one week. A 25%-50% permanent demand increase is not viable.

It is unlikely that gas prices will increase massively – and also unlikely that we will build more pipelines. Data centers construction will stall before policymakers allow largescale price impacts

Higher energy prices are deeply unpopular – as is the construction of new energy infrastructure. Putting new pipelines in is almost impossible. Putting new power lines in is even more difficult. Without new transport infrastructure, power and gas prices will rise. Local opposition to new construction will become fierce as this proceeds. Expect more states to block data center construction as a result.

The only real paths here are as follows:

1. Data centers continue to build at the planned pace, power and gas prices rise nationwide. This is unlikely because policymakers will begin to block data center builds as constraints cause price increases

2. Natural gas pipeline build-out proceeds to support data center build-out. This is unlikely because getting pipelines permitted has been nearly impossible in the US. Any attempts at eminent domain will be crushed in courts until a climate-concerned friendly administration is in power, and then it will be crushed in the federal government as well

3. Data center build-outs are stopped or slowed at a state level. This is highly likely. Local politicians will be rapidly voted out if energy prices rise rapidly

4. Data centers become more energy efficient. This is a possible scenario whereby the AI systems being developed become more efficient and the existing data center infrastructure thus also becomes more efficient. Direct analogs include the fiber optic over-built of the 1990s whereby we over-laid cable and had excess capacity for 20 years. This is seen as a major possibility as AI systems move from brute-force LLMs to more sophisticated and distilled models. Existing data center capacity would continue to meet expanding needs as AIs get more efficient - allowing more time to expand energy distribution systems without spiking costs

5. Data centers build directly on top of natural gas production sites or develop new power procurement methods. This is quite possible and most data center developers have large teams to address this - but from what I’ve seen most of their teams have no real understanding or experience with energy infrastructure. In other words, I’m skeptical. In addition, tight gas like we have in the US peters out after 10 years - a major mismatch with a co-located data center that is meant to last 20 years.

Conclusion: Natural gas distribution constraints will put brakes on data center development

Demand for data center components won’t hit projections unless we can expand pipeline capacity. If this starts happening, I’m going to be investing in traditional pipeline builders and operators. I don’t count on it happening, and so I expect data centers to hit a hard wall in terms of capacity expansion in the US and the rest of the world.