May/June Newsletter - Changing Policy Considerations in Clean Energy Investment

May/June Newsletter

I usually don’t put my newsletter up as an article - typically the newsletter contains a level of detail that isn’t meant for a general audience. But this month’s newsletter covers several major economic implications should they come to pass - chief amongst them the changing cost of capital from higher US debt.

The newsletter:

This month’s newsletter broadly applies to the energy sector as well as H2. In the past month major lawsuits, rulings, legislative, and federal changes have created waves of uncertainty to affect most investments and projects. While this is an H2 investment newsletter, the content broadly applies across all energy infrastructure. The escalating uncertainty means that most long-term investment dollars will pause for several months and that now is a time to look at product strategy and project strategy.

Long term investors are generally looking for risk-adjusted return, and the current escalation of uncertainty has placed risk beyond the potential returns. Risk has ballooned across energy sectors in addition to within each sector - meaning product strategy and risk within one sector and compared to adjacent and competing sectors is entirely unclear. Rapidly changing and unresolved policy moves risk-adjusted returns on many projects in the negative until more certainty is reached – either in courts or in final legislation. Money should be parked in low-risk investment until at least some of the current policy issues are worked through.

Now is a good time for companies to game out what potential outcomes of these major policies are for their products, projects, and portfolios– and how their product and investment strategies can respond quicker than anyone else at each resolution.

Escalation of uncertainty across all energy infrastructure

In the last newsletter I detailed how the stymying of the DOE Hydrogen Hubs was not all gloom and doom. In the midst of those mega-projects slowing and stalling, I was seeing opportunities for smaller projects to move forward outside the shadow of these giants – and getting advisory contracts with some. Smaller projects mean more investment opportunities for outsiders – because it is much easier to invest directly in a small project or in the related supply chain than it is to invest in a project run by a hundred billion dollar conglomerate.

In the interceding weeks, much larger and more significant changes have come to the energy investment landscape. Many if not all infrastructure development projects are slowed down or otherwise impacted, not just hydrogen. The major drivers, roughly in order of importance, are:

May 21 - The proposed gutting of California’s (and 40% of the US) ability to regulate vehicle emissions – and then use that precedent to eliminate all state emissions regulations in other sectors such as power. This could affect all clean energy in the US for years

May 22 - The proposed budget that will add an estimated $2.*T to the deficit will push up all cost of capital, making high-CapEx projects more expensive – This longer-term effect will push a lot of clean energy projects into being relatively more expensive as they are more CapEx intensive – and push projects to move forward before cost of capital increases

May 22 - The attempted cancellation of 45V and much of the IRA – this will immediately stymie the growth of clean H2 owing to many projects being unprofitable without the tax credit

May 29 - A lower court saying that Trump’s reciprocal tariffs are not constitutional – and then a court of appeals temporarily reinstating them – This will pause H2 projects until price certainty comes as most of the H2 equipment comes from overseas. If the tariffs remain in place, it will add many months for procurements teams to re-vet and re-price their supply chains

May 29 - The Supreme Court voted 8-0 to scale-back NEPA – National Environmental Protection Act – This mostly affects the Hydrogen Hubs in H2 and any other projects receiving federal funding– and has positive implications if 45V construction start date is extended by a year or two. It also will affect federally supported pipelines and grid expansion

Why these federal and judicial changes are critical for clean energy infrastructure

Details matter. Some of the implications are directly clear without details. In matters of law and policy, details can entirely change the outcome. Given that every product and project is competing with other current and future technologies, a seemingly small change will have large impacts on project or investment viability.

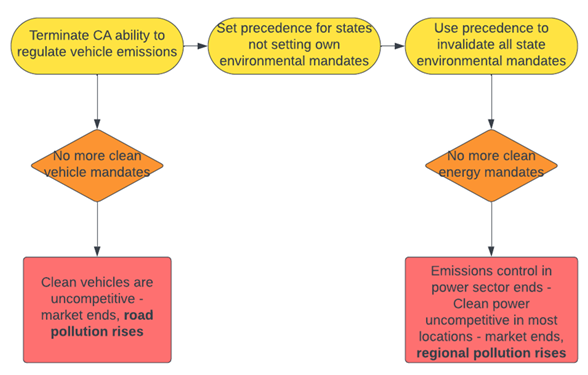

Gutting of California’s ability to regulate vehicle emissions

On May 21 the Senate overturned 50 years of precedence to use the Congressional Review Act to overturn California’s waiver that allows CA to set more stringent vehicle emissions standards. California enacted a ban on tailpipe emissions to phase out sales of new gas power vehicles by 2035 with the aim of getting all gas powered vehicles off the road by 2050. 17 other states follow California’s alternative rules. Together these states account for 40% of the US population. The size of this market would dictate that most vehicles end up following this rule, because designing two separate factory lines to have one low-emissions cars for clean states and another high-emissions car for other states would be expensive. The end result is gutting of clean emissions standards. That means:

Tailpipe emissions increase in cities and states that have had serious problems with vehicle pollution in the past, with serious health effects and decrease in average lifespan as a result

No more moving down the cost curve for low emissions vehicles in the US as the US manufacturers reduce their clean vehicle development and production

the rest of the world continues moving down the clean vehicle cost curve, eventually hitting and surpassing break-even without us

If the US manufacturers fail to follow suit with new cost-effective clean systems, US cars are no longer competitive in many use cases

This leads to the slow death of US manufacturers that fail to adapt

While this has happened in the past (Trump stripped the ability in his first term in 2019, CA and other states sued, and the issue resolved when Biden reversed Trump’s executive action in 2021), there is a major larger goal here: get it to courts, set a precedent to strip states rights on vehicle emissions, and use that precedent to also strip states of their ability to regulate all emissions – including power sector emissions. This would reduce the need for pollution controls on power plants. Without the need for costly equipment to reduce pollution, fossil power becomes or remains lower cost than nearly all clean power sources. The direct impact is that most clean energy projects become less competitive, and investment in clean energy is reduced or grinds to a halt.

The risk here is so major that until this is resolved, building new energy of any kind has significantly added risk. A project built under current strict emissions controls would result in costlier power than a future fossil project built with more lax controls. The project built under strict controls would find itself out-competed on price by new projects. Energy projects generally take one to two decades to pay back or capitalize their CapEx– if there is a prospect that regulations drastically change to allow new entrants to undercut them on price, future cashflows are in jeopardy. That project could become a stranded asset. The lenders lose their capital. So today it is risky for lenders to move money until there is at least some more clarity here.

Likelihood of this happening: It’s entirely unclear to just about everyone how the courts will rule on this. The Supreme Court has shown that they will rule in favor of states rights on many issues, but this may be an exception since they’ve also shown they will adhere to conservative principals over states rights in many cases. Moreover, even if the CA waiver is eliminated for cars, the case for emissions controls in other sectors would need to go through another set of cases and could have a different outcome. There are also many other ways this could play out, and several other major goals the waiver cancellation intends to accomplish.

A major exception: Even with all these issues, export opportunities of clean H2 derivatives look strong in the long term. The EU and the rest of the world appears to be moving forward with clean energy, so exports of clean fuels remain in demand. Planned investments can move forward regardless of the outcome with states rights to set their own emissions standards.

The proposed deficit budget will increase the interest on Treasury bills – and thus increase the cost of capital of all projects –pushing many out of FID

Pushing to move faster to market is the potential debt increase from the proposed budget. The increasing cost of capital from a rising US debt would push projects to invest sooner before the cost of capital increases – particularly for high CapEx projects.

This is a very tough concept to fully grasp – but high CapEx/low OpEx projects are more sensitive to higher cost of capital than low CapEx/high OpEx projects. Clean energy tends to be the former, fossil energy can be moreso be the latter – especially if emissions controls are relaxed.

Commercial capital projects often capitalize their CapEx over a timespan of 20 years – some go lower to 10 or 15 years. The proposed budget deficit is causing the interest rate of long-term treasuries to rise. 10 year treasury bond yield rates are the benchmark for the “risk-free rate” of return. The risk-adjusted ROI for capital projects must exceed this risk-free rate of return by an amount determined by the company – and as the long term treasury rates rise, the required ROI for a project also increases. Most energy projects are low-margin, meaning they often are just above the required ROI to build. A 1% increase in cost of capital over 20 years would result in an 8% increase in the CapEx contribution to the LCOE of energy for a project – in many cases reducing the ROI below required margins. A project that doesn’t meet margin requirements doesn’t get funded.

Product and Investment Strategy - CapEx vs OpEx sensitivity

A low CapEx project would not be as affected by a higher cost of capital and would become more competitive relative to a high CapEx project.

The important part is CapEx Sensitivity of projects to higher cost of capital. CapEx is incurred at the start of a project before any outputs are sold. The CapEx is paid off by cash flows after commercial operations start. These cashflows are are discounted over time – and several years of compounding discounting has already occurred between construction start and commercial sales dates. OpEx occurs after commercial operation starts, roughly simultaneously with income, and is discounted at the same rate and at the same time as the associated income. As result – high CapEx projects with several years of construction will have future associated income cash flows heavily discounted. As a result, as we see in the chart above, higher cost of capital increases CapEx portion of the cost stack. Another way of looking at this is that CapEx is incurred at the start of a project when the value of money is at the highest – but doesn’t start getting paid back until the project actually produces cash flow in the future when money is worth less. A higher discount rate means these future cash flows are even further discounted to be worth even less, so the price of the sold goods needs to be increased to make up for it. The OpEx portion of the cost stack is significantly less affected by a higher cost of capital.

CapEx intensive projects with all up-front cost – like renewables– will see a 5-10% greater increase in LCOE/LCOH from a 1% increase in cost of capital compared to a project with much lower CapEx and much higher OpEx. This means that high CapEx projects will become more disadvantaged with higher cost of capital. This will affect all energy. Renewables, vertically integrated electrolytic hydrogen, nuclear, batteries, and hydro are all high CapEx, low OpEx projects. Nuclear has the longest construction times – and thus the largest cash flow discount between cost incurred at construction start and the income produced at commercial operation start – and will be affected more than most other projects.

This potential outcome has a major interaction with the attempt to strip states of their rights to set emissions standards. If the courts strip away emissions controls, fossil power plants become comparably low CapEx high OpEx projects. That 5-10% lower LCOE they can achieve in a higher cost of capital regime will make a big difference. Even without stripping away emissions controls, the outcome of higher cost of capital will favor existing and many new-build fossil plants with their lower CapEx to OpEx ratios.

Cancellation of 45V and other parts of the IRA makes clean H2 and the supply chain less economic

45V is effectively cancelled for most projects under the budget bill recently passed by the house. To qualify for 45V under the proposal, a project must start construction before the end of 2025. Most projects will not hit FID by then – making them ineligible to start construction and qualify for the credit. Exxon’s Baytown is likely the only major project that will qualify if the budget goes unchanged through the Senate negotiations.

Over the 20-year lifetime of a project, the value of the $3/kg for renewable H2 works out to ~$1.70/kg (only half of the operating time of the project would get the credit). For clean reformation H, the numbers work out to be $0.40/kg to $0.70/kg over the lifetime of a project.

While the cutting of 45V will reduce clean hydrogen production – the major loss comes in the reduction of the equipment cost on the electrolytic side. The electrolysis space is extremely immature – with no standardization or modularization of core equipment or balance of plant. Rapid expansion in the space would have driven the total installed cost of electrolyzers down to competitive pricing in some regions without future government support. 45V would have positioned the US at the forefront of renewable hydrogen development. Without it, the US cedes this to the EU and China.

Reformation hydrogen will not be moving down the cost curve for the most part – all the technology involved is mature, with the exception of pyrolysis. In terms of future value, this is less of a loss. In terms of emissions reduction, however, the effective cancellation of 45V it remains significant loss.

Reciprocal Tariffs Constitutionality

The flip-flop of the reciprocal tariffs puts equipment buyers in an impossible position. Importing equipment at high tariff rates that could suddenly drop after import would mean a future competitor would have advantageous pricing for the exact same project. This means money can’t move until we have clarity on tariffs. Even then, a large change will result in slowed projects – sourcing and vetting new suppliers is a significant task that takes both time and money, further slowing projects.

Deeper in the clean energy equipment supply chain, tariffs will also determine who is onshoring manufacturing into the US. Manufacturing here could get around final import tariffs – but introduce tariffs and higher costs for any components that are imported for manufacturing. This is a knock-on effect that will affect investment and product strategy across all energy, not just clean energy.

Scale-back of NEPA

This change is the only one in this list that provides a large risk reduction for projects and investments.

The National Environmental Protection Act (NEPA) analysis is required by any projects receiving federal funding. The analysis and permitting is onerous in both dollar cost and in the time. NEPA slows down a project by at least two years if a project accepts government funding.

Now, the Supreme Court unanimously ruled that NEPA only applies to the environmental impact of the project itself, not upstream or downstream environmental impacts. In the past, opposition has used upstream and downstream impacts to stop projects. Building a coal plant, for example, would be stopped by suing for the coal plant to assess and mitigate the environmental impact of mining the coal they use for the plant, effectively placing responsibility for the entire supply chain on the plant developer and not the coal mining company. The amount of analysis and mitigation required would kill projects. With the new ruling, the coal plant would be responsible for only the pollution produced by the coal plant.

The scale-back of NEPA should significantly reduce the cost of accepting federal dollars for a project and also accelerate project timelines. If the 45V construction deadline was extended only two years, this reduction in NEPA timelines could make it so the H2 hubs would be able to get in under the deadline.

More broadly, this change will make it much easier to build pipelines (hopefully hydrogen pipelines), grid infrastructure, and transportation infrastructure that will be required for the energy transition.

How to survive and thrive in this environment

Many of these uncertainties will be resolved in the coming months. The courts are taking many of these cases as emergency actions – moving them ahead of the queue to reach clarity more quickly. The quickest of these will take several months to resolve – unless the new budget moves faster than predicted. In the meantime, revisiting strategy to be prepared for outcomes of these changes will be paramount to success. Whoever moves smart and fastest will see the best returns. Choose your partners and your help wisely.